Expected Returns and Risk

Volatility, Beta, Momentum -Tools to understand mutual funds

This blog is somewhat close to me as I have been trying to understand what makes a few mutual funds tick. In the process of doing so, I have learnt something and I had to write down the same. I hope this write up explains my understanding. I do hope that eventually we can explain a few mutual fund behaviors and possibly also strategizing on fund selection. To that extent, this will be a multi part blog. This particular one may be a bit more mathematical for my liking but I do believe may be essential for us to know. I will link the other blogs here eventually.

Arithmetic and Geometric Averages.

In the area of investing, it is important to understand the difference between arithmetic mean and geometric mean. Take a simple example of 3 years returns of 10%, 0% and -10%. The arithmetic average of these returns = (10%+0%+-10%)/3 = 0%. We expect to be back to our original NAV. Fact is we get multiplicative returns.

Our NAV path will be as follows:

Basically we end up at a lower NAV than predicted by arithmetic mean. We obtain what are called geometric returns which a lot of people also call compounded annual growth rate (CAGR). In this case, geometric returns = -0.33% and is obtained as

CAGR = ((NAV_final/Nav_intial)^(1/N)) - 1

where NAV_final is the ending NAV and NAV_initial is the starting NAV. N is the number of years.

Arithmetic Mean >= Geometric Mean is a mathematical reality and this means we will always obtain lower returns than by simply averaging. Also the equality in the above equation happens when all numbers are equal. The Geometric mean approaches Arithmetic mean when the non uniformity of the various elements reduces. That is to say, the lower the variation of returns, the higher the geometric returns. For a given “average” rate of return, we seek lower variation of returns over time.

Volatility

All data on NSE indices from their webpage. The calculations are mine.

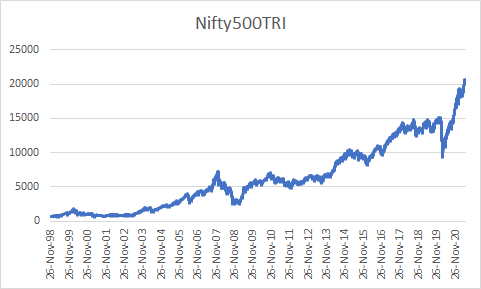

Below is chart of Nifty500 over the last 22.5 years.

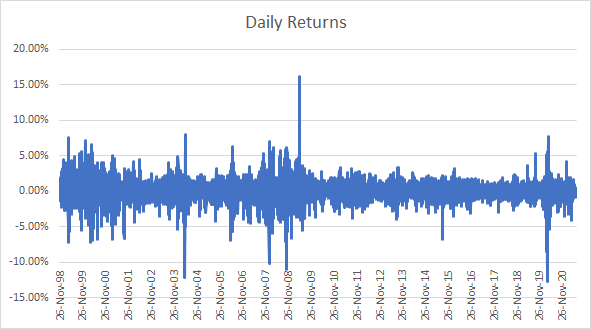

If we compute the daily returns of the index over time, we see the following

There is a huge daily return variation and this variation is itself, as discussed above, is not preferred. In fact if we plot a histogram (graph of count of daily returns),

As can be seen from the graph above, it is *almost* equally likely to see returns around 0.07% (which is the arithmetic mean). The above style of graph was first discovered by the great mathematician Carl Gauss and is called Gaussian distribution. We come across this in many walks of life. It is therefore even called “Normal” distribution. It is equally likely that you may returns on either sides of this arithmetic mean on any given day. That is pure luck. This is also the noisy-ness of the daily returns we experience in the stock market. Some people call this randomness as

Random Walk. . Note that the distribution is not really normal by a few metrics. But, it is a close approximation.

For a normal distribution, there are two important parameters: mean (mu) and standard deviation (sigma) . Knowing these, the complete distribution could be made. The mean is the arithmetic return many would expect (wrongly!). But, due to the sigma, we will see a difference in returns from mean over time. This geometric return for normal distribution is derived as GM = mu - 0.5*sigma*sigma.

The term sigma is called volatility by many folks and as can be seen from the above, sigma can drag the returns lower and many finance folks call this reduction in returns as “volatility drag”.

While the causes of volatility are not understood, it reasons that if there is lack of clarity on future prospects of the business, there can be a dispersion in people’s expectations of future returns resulting in stock price volatility.

Beta

Stocks are an incredibly correlated asset class. Many times, stocks go up together and down together. Say a stock has a correlation to Nifty50 (index) of 100%. We call it a beta of 1. If the index moves by 10%, the stock moves up by 10%. If the index falls by 20%, the index falls by 20%. If on the other hand, a stock has a beta of 2, if the index rises by 10%, the stock rises by 20%. Similarly, if index falls by 20%, stock falls by 40%.

As can been seen, beta increases the average return of a stock (v/s index) but also increases the volatility of the stock (both go up by 2x). So while intuitively we expect higher returns as the beta increases, unless the underlying volatility is low, we may see a drag in performance as the beta increases. Below table explains this. As the beta increases, returns increase up until a point before they start worsening.

The reality is that most stocks have an independent volatility apart from correlated volatility to the index. For example, Hero Motor is a big company in Indian economy. It is likely that its revenue and profit performance is related to multiple things such as economic activity in India, auto sector correlation, interest rates and it owns “idiosyncratic” risks due to company specific risks. So a stock can have multiple betas and its IVOL (idiosyncratic volatility).

All of this is to say that the path of a stock may not always be straight up but can have a lot of drag and this drag, if can be smoothend, it will be great choice of stock selection. Mu is simply the “Expected” return and we want stocks to have higher expected returns with lower volatility. Also, if a portfolio has two stocks with equal expected returns but different volatility, we can enhance the portfolio return by simply dropping the higher volatility stock as the combined returns will be lower. Another approach could be to give higher weight-age to the low volatility stock and less weight-age to higher volatility stock. Many follow this and call it volatility scaled portfolio.

Momentum

In 1993 Jegadeesh & Titman published a paper which formalized that momentum is a good way to pick stocks. Stocks which have gone up recently will continue to go up in the near future is the basic conclusion they drew. In fact, we now have data to prove an almost monotonic behavior over time, between recent past winners and future returns. It is in this context that we can say that momentum stocks have “higher” expected returns than the index. A combination of momentum stocks which exhibit low beta or low volatility can be a great portfolio.

Nifty Strategy Indices

NSE maintains and publishes “strategy” indices that capture the essence of these points above. We do have a NiftyLowVolatilty50, NiftyHighBeta50, NiftyAlpha50 and NiftyAlphaLowVol30 indices. Each of them picks stocks from as subset of the Nifty500 universe. The NiftyLowVolatility50 index invests in 50 lowest volatility stocks. The Nifty Alpha50 invests in Momentum stocks while NiftyHighBeta invests in highest beta stocks. The NiftyAlphaLowVol index is a portfolio of high momentum and low volatility stocks. You can read more about them here

These portfolios have been back tested and the results are available for us to understand more. A portfolio of stocks buying low volatility stocks consistently has beaten the index whereas a portfolio of consistently high beta has failed miserably and has probably unperformed FD investing with much higher volatility. Similarly a portfolio of momentum winners has done better than the index whereas a portfolio of momentum winners with low volaility has delivered better “predictable” returns with lower drawdowns

A summary of these 16+years back tested daily returns data is

We can infer that the low vol portfolio has similar expected returns but outperforms the broad market due to its lower volatility. The higher beta on the other hand suffers from higher volatility as well as lower expected returns. Interestingly, the final CAGR for the momentum + low vol strategy is similar to the pure momentum strategy despite a 1.5% annually lower expected rate of return. This is because of its lower volatility.

A simple strategy to drop the 50 stocks which are in the NiftyHighbeta50 portfolio from the Nifty500 portfolio could boost the returns for the portfolio. Note that both beta and idiosyncratic volatility are time varying. It is possible that a high beta portfolio does well in the short term but in the really long term, when one major down happens, the portfolio may never recover. Below shows that the High beta stocks were laggards but not bad up until end-2007 and from thereon, they fell more than the index and never really recovered after that.

I submit that we must have these indices (along with Value) as our benchmark indices handy to discover what the strategy of a mutual fund manager is.

We shall be exploring this in the subsequent blogs.