Investing Outside the Index

Momentum Investing and Mutual Funds

In the previous blog, we saw that many mutual funds barely beat the index. But we do notice that some funds continue to perform better than the index, even over the long run. Today we explore one of many ways to invest outside the index: Momentum Investing.

Momentum investing is, as the name indicates, about momentum in stock prices or businesses. The most popular type of momentum portfolio is “Price Momentum”. The basic thesis of momentum (esp. Price Momentum) is that an asset that has performed well(badly) in near term (say 12 months) will continue to do well(badly) in the upcoming future month/term. Hence the term “momentum”. The academic momentum strategy suggests that we go long (i.e., buy) the “Winner” stocks and short (i.e., short sell) the “Loser” stocks. This portfolio, updated frequently can provide a performance that is different from the index (not necessarily better than index but different from the index)

The essence of momentum in stocks/assets is like sportsperson “form”. When a team/player has been exhibiting top form (Joe Root in cricket today), they are expected to continue to play well in the next innings/game. Similarly, a player with bad form (Ajinkya Rahane currently in Indian team?) is expected to under-perform in the next innings/game and hence there are calls for the player(s) to be culled from the team. For players in the top echelon of sports, this is not supposed to happen as they are projected to provide their best performance anytime (statistically speaking, every player’s each match performance is independent of the earlier match). But many do believe in this hypothesis and hence this can be counter-intuitive for many to accept.

The literature on momentum is deep1. I would encourage readers to read various books2/blogs3 listed below to learn more. The details on the history of momentum and the nuances of various practitioners can be read through various blogs/books. I shall try to summarize the basic process below.

Define your universe of stocks. Typically, you would have filters on volume of stocks traded /market capitalization etc. In Price momentum, you pick stocks which have moved up the most in the past 12 or 6 months. Pick the top decile (10%) of stocks from these. This basket of stocks will be held for a month. Repeat this cycle every month at the start of the month. This simple process is the most popular form. There are variants based on look back period (3 months, 6 months etc.), weighting process (market cap weight, momentum weight, Sharpe ratio weight, equal weight), volatility screening (remove high volatility stock) and rebalance frequency (6m, 3m, 1m, 1wk). The main point is you sell the losers and buy the winners mechanically. There is evidence in both India and many other countries that this process has given good diversification outside of index as well as better performance from time to time against index.

It is important to note that most versions of these implementations will result in “similar” performance outcomes. The NSE indices also include the NiftyAlpha50, NiftyAlphaLowVol30 and Nifty200Momentum30 as different flavours of momentum stock indices. You can read on their stock selection process here. Below graph captures the performance of momentum vs broad market index4.

As can be seen, the orange line is almost always better than the broad market. This is what makes it very interesting. A strategy of buying the winners seems to really generate excess returns. The methodology is also mechanical in nature (in world of finance, they like to call themselves quantitative). For those interested, the above performance difference is an excess difference of ~6.4% per annum. That can generate significant wealth over a long term.

I suppose readers of this blog are not really interested in this academic stuff. We are interested in the investable mutual funds which are momentum oriented. We discovered earlier that Axis Long Term Equity Fund is one such. I argue that Nippon Small Cap Fund, SBI Small Cap funds are momentum-based funds too.

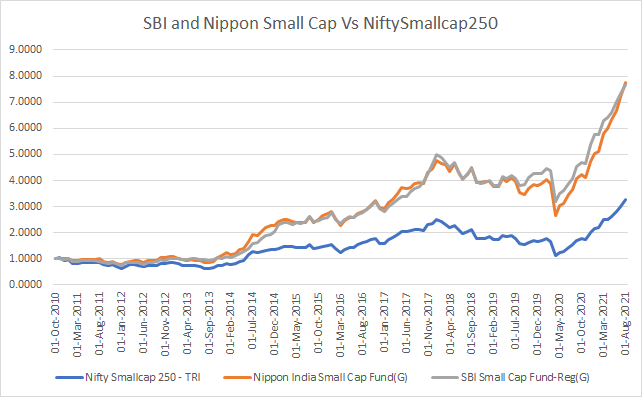

We start off with the comparison against their index. Clearly, they have been different to the underlying index and mostly have done better than the index.

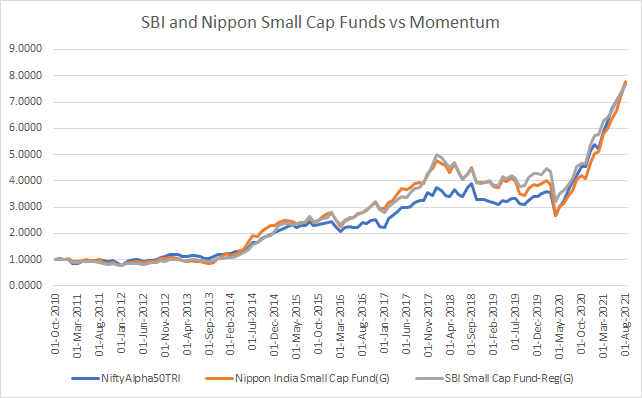

We now compare them against the momentum index.

Firstly, it must be obvious that the funds are noisier versions of each other. Choosing the two funds as part of diversification of managers would not work. There are times when the funds have done better than the index. We analyse them in different durations and below plots show the same.

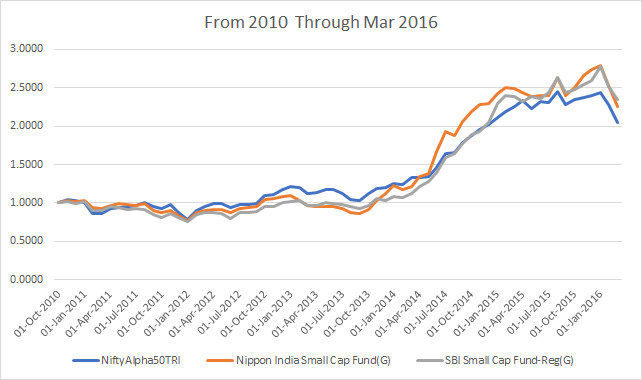

Basically, for a brief period, the funds did better than the momentum index (Mid 2015 through early 2016) but otherwise, the funds are momentum oriented in their performance.

It must be noted that while the funds are momentum oriented, there are possible differences clearly emerging over the last year with slight underperformance relative to the index. It must be seen if this continues. The fund managers do not specify their stock selection process. It is possible they may underperform in future under the weight of the cumulative assets gathered like described here.

Conclusion

Momentum stock investing buys into stocks that have recently done better than their cohort (assets or stocks). This strategy while has high turnover (monthly rebalance), provides performance differentiation to the broad market.

Nippon Small Cap Fund and SBI Small Cap mutual fund schemes have thus far been momentum oriented. Investors can choose to invest in the scheme but with the clarity that they may deviate from the index soon. I would recommend yearly performance comparison against the NiftyAlpha50 index. If the difference is large, move out of these funds. The two funds are con-joined twins. Invest in only one of them.

“Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency” by Narasimhan Jegadeesh and Sheridan Titman

“Stocks on the Move: Beating the Market with Hedge Fund Momentum Strategies” by Andreas Clenow and “Quantitative Momentum: A Practitioner's Guide to Building a Momentum-Based Stock Selection System” by Wes Grey and Jack Vogel.

https://alphaarchitect.com/blog/ and within India, https://www.portfolioyoga.com/wp/ by Prashant Krish.

Data from https://www.niftyindices.com/reports/historical-data