Glorified Asset Allocators

Parag Parikh Flexi Cap Fund Review

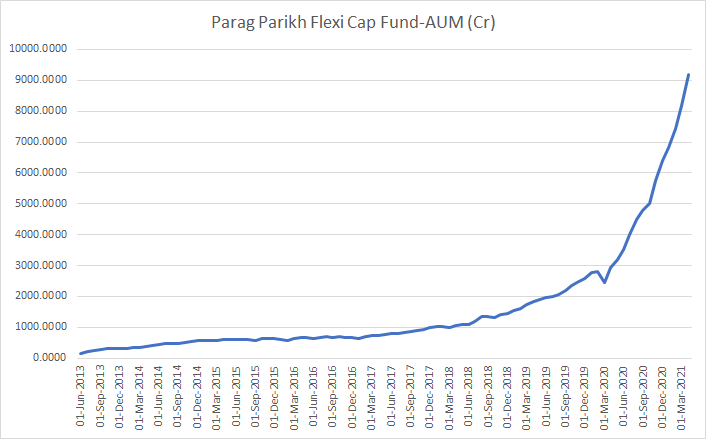

Today we shall review the Parag Parikh Flexi Cap Fund. It has been a fund that has captured a lot of people’s attention. The fund manager used to run a PMS scheme and over time decided to convert all account holders to the mutual fund. The fund started small and has been collecting AUM at a great pace. Indeed from NFO to now (Jun 2021), the AUM has grown from tiny 152Cr to now almost 10000Cr. Here is the AUM chart over time.

There has been a exponential growth in AUM esp since the pandemic began with a ~3x growth in AUM since Jun 2020. Clearly, the fund has caught people’s fancy recently and is investors are piling into the fund. A quick check on Valueresearch website shows that scheme is now in the top decile of Diversified Equity Fund category by AUM. This recent tripling of AUM brought the fund to my attention and I thought I must review the fund.

First a few details. Below snapshot is from the AMC’s website.In their own disclosures, the fund managers disclose their personal holdings and highlight the same.

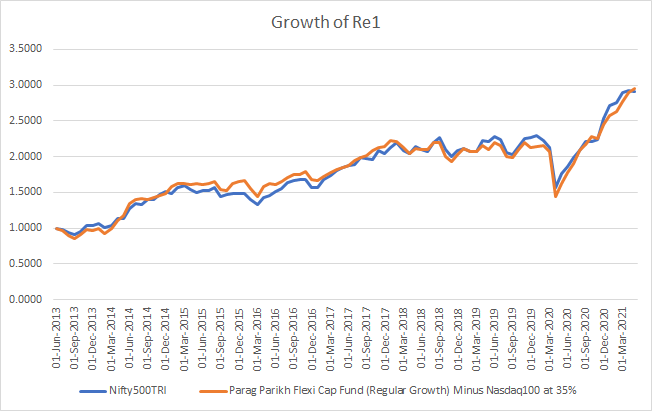

How about the fund’s returns? I chart below the performance of the fund against the Nifty500TRI index.

The fund has clearly done far better than the broad index and as the graph above shows, the spread is widening indicating “alpha”. This is probably what has been driving increased attention and AUM to the scheme.

Full details of the fund are here. The very first few sentences catch your attention. Here is the snapshot

The details further talk grandiosely about having three different fund managers one each for Indian stocks, foreign stocks and domestic debt. So first off, the fund should not be having the Nifty500TRI as a benchmark. In fact they even have an “additional benchmark” and even that does not have a benchmark which matches the actual portfolio allocation.

A close look shows that the fund has consistently been investing into NASDAQ listed stocks with big names such as Microsoft, Facebook, Google etc. I think it is appropriate that we compare the fund against the Nasdaq100 index. Within India, we do have the MotilalOswal Nasdaq100 ETF. I track the monthly NAV and below is what we see.

Clearly, the Nasdaq100 has had a glorious past few years and any allocation to the Nasdaq100 is going to accrue to the investor.

How about we create our own index which is a composite of the Nifty500 and the Nasdaq100. We start with a 65% and 35% allocation to Indian and Nasdaq100 indices. At the end of every month, we rebalance to maintain the ratio. This is what I see.

WOW!, we actually replicated the entire fund monthly NAV just by recreating the index. There is ZERO work actually being done by the fund manager. Another way to say this is the fund managers are glorified automatic rebalancers. They are truly not adding any value worth their expense ratio.

Of course, this is harsh considering that a lot of people consider Mr Rajeev Thakkar a great fund manager. But data cannot lie. Let us create a new NAV which is Indian stocks NAV by subtracting the Nasdaq100 performance to see if Indian stock allocation has alpha. We shall adjust the weight-age back to 100% by scaling to 65% allocation. Here is what we see

As was expected, the Indian equity allocation is also a closet index. What is important to see is that even at an AUM of 150Cr, the Indian book is exactly replicated. It is not because of the new high AUM that the closet bench-marking is happening. This has been the case since inception!

So what does this mean? The three fund managers are essentially deciding how much to invest into the two indices and definitely are not adding any value to their unit holders. They are hence only broad asset allocators and charging annual TER for the same. The fact that this mixing of assets is hiding the fund manager’s real value add (or lack thereof), coupled with not mentioning this modified index as their additional benchmark leaves a bad taste. We must question their intentions.

One advantage of the discovering the true nature of the fund is that you can expect this behavior to persist at scale (they are just index pushers). What can be a problem going forward is if the Nasdaq100 underperforms, this fund may not be worth it.

My personal advise. Do not invest in the fund. Speak to your advisor on appropriate asset allocation between Indian and foreign stocks and select appropriate index funds.

Couple of points:

1. Chosing 65:35 ratio as benchmark while knowing that 35 was their upper ceiling in foreign stocks and they were always lower than this is an issue. Because nasdaq100 has done better it shows benchmark in better light. On real benchmark (like 75:25) they have generated alpha. This is like bending the data to show what you want to say

2. Only Indian stocks have been compared to nifty500. But foreign stocks return has not been compared to nasdaq 100, why because it has created alpha over nasdaq 100. Omitting data to show the narrative one wants to

3. Regular fund have been chosen, which has an expense ratio of ~2% so even the optimal chosen benchmark has been beaten by 2% before fees. So fund manager has done some work.

4. Indexing also comes at a cost so indexing by oneself will not have the same return as the optimal benchmark but lower than that

I dont think a retail investor can rebalance everymonth. and can you explain how they able to reproduce average of two indices with 40 only stocks. i think this is bad article which is based on your biases