Momentum Variations

Momentum and Low Volatility

In an earlier blog post, we looked at momentum investing. There is compelling evidence that price momentum does seem to affect stock prices, and a strategy that consistently buys “winners” can beat the market. While momentum investing works, investors have tried to “improve” on momentum investing. One of the most common methods to do the same is to combine low volatility investing with momentum investing.

For instance, in this blog, the author shows that the majority of momentum returns in the 2003-2007 period accrue in the short leg (selling losers), and hence “excess returns” to the long leg of momentum strategies are lesser. The author suggests that using excess returns/ volatility (like the Sharpe ratio) seems to have been a better signal to capture momentum returns than just excess returns. USA markets have not provided long-only “alpha” in the last 10 years despite the popularity of momentum investing but mixing with low volatility has helped provide better returns. And that should be a somber reminder to people on how efficient the market is. Momentum is an anomaly (in that we do not know why it happens) but, since its discovery, the returns of momentum portfolios have been steadily declining as the market has priced in momentum stock’s performance. Luckily, the same blog also shows the author’s calculations indicating that momentum when combined with low volatility still provides continued out-performance (esp. for the long leg of investments).

On the other hand, this blog shows the impact of various styles of combining momentum and low volatility and how it has pared in USA markets. With similar thoughts, even in Indian markets, we have four different types of momentum indices from the NSE team at niftyindices. The following are the indices and their various

Nifty Alpha 50: Price Momentum based. This strategy selects stocks purely based on price. Unfortunately, no index fund tracks this. The components of the index are illiquid and may not be easy to implement at a mutual fund level but individual investors *may* attempt replication. We also discovered that there are alternatives in the active mutual fund space.

Nifty Alpha Low Volatility 30: Combination of Price Momentum and Low Volatility. In this, you separately sort on momentum and volatility and add the ranks to select the final list of stocks. There is ICICI Prudential Alpha Low Vol Fund that provides a low-cost option to invest into.

Nifty 200 Momentum 30: This selects stocks based on their risk-adjusted Momentum (like Sharpe ratio). There is UTI Nifty200 Momentum30 fund which provides a low-cost option to invest in this strategy.

Nifty 100 Alpha 30: This selects stocks based on “Residual momentum” and sorted by “alpha”. There is no fund yet that passively invests in this momentum strategy.

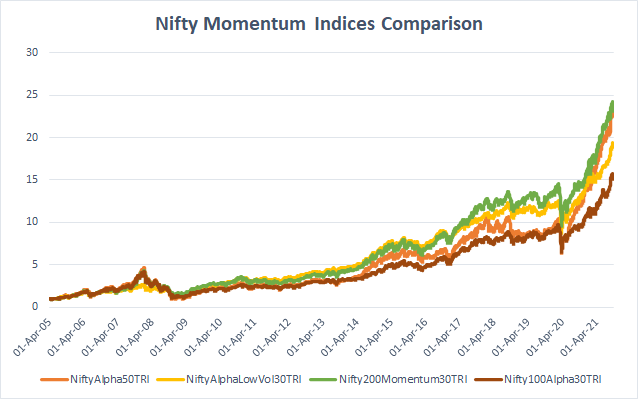

Over the last ~16.5 years, all of them have provided similar returns as is seen below. It is interesting to note that the Nifty100Alpha30 has been a slow performer compared to others. One reason for it could be the universe of stock selection. The Nifty100 selects momentum stocks based on the large-cap universe whereas the other indices have midcap and small-cap coverage. If this is indeed true, we can say that momentum is a stronger phenomenon in small and mid-cap stocks than in large-cap names. This should tell us that there will be a limit to the size/capacity of this strategy.

Moving to drawdowns, they are different.

The amount of pain one would have to undergo sticking to the pure price momentum strategy is difficult to imagine with 80% of the portfolio lost. In fact, the large-cap-only momentum (Nifty100Alpha30) also has crashed similarly at various times. Interesting to note that in any combination with low volatility, the draw-down and recovery were faster. You will see that during the financial crisis period of 2008, the combo recovered its entire losses within a year whereas the other two strategies took 6 years to recover the initial losses that started in 2008.

The fact that one may not endure 30-40% if not 80% drawdown is reason enough to not invest in momentum strategy. In fact, this very reason is why momentum generates its excess returns as investors stop investing when they see such large losses in their portfolios.

This blog will not be prescriptive in suggesting which style of momentum is better. I would simply say that the combination of adding low volatility to momentum is a clever idea. Raw price momentum may make it difficult to stick to. Hence, the intention might be correct for looking higher returns, we may not achieve the same as we switch out of the style at the wrong time. This is called the “behavioral gap”

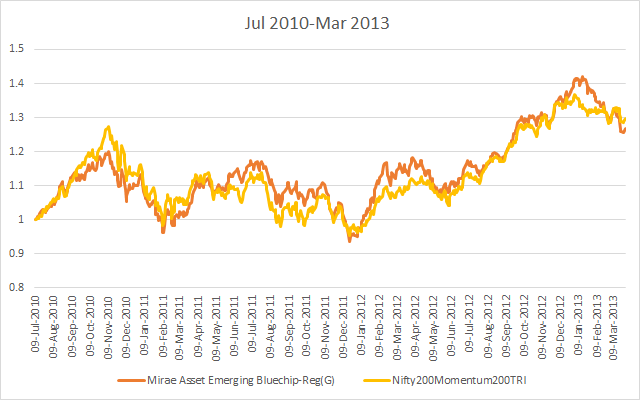

We end by looking at an active mutual fund that is inclined towards the Nifty200 Momentum30 Index. Mirae Asset Emerging blue-chip fund is categorized as a “large and midcap fund.” This is a Flexi cap fund.

But, if you compared to the Nifty200Momentum30 Index, we see a near fit.

This is a near-perfect fit. The fund has served the individual investor by giving them access to the momentum strategy. But, now that we are aware of the style, we might as well consider moving to the UTI Nifty200Momentum30 Index. It is a lower cost and better transparent strategy, and the fund manager may not change styles later.

Conclusion

Momentum strategies can have horrible drawdowns and may be tough for investors to live through. Beware of investing in momentum strategies. Living through these massive portfolio losses may not be easy for an individual’s health.

Momentum strategies work better with low volatility combined. This helps to reduce volatility which helps the ability to stick to the investment process and reduce the behavior gap. While drawdowns can reduce, they may still not be sufficient to fight investor withdrawals at inopportune moments.

Mirae Asset Emerging Blue-chip fund is a momentum fund. For new money, invest in the UTI Nifty200Momentum30 fund. For already invested money, consider suitability to move to the index fund based on taxes.